Loan Eligibility Analysis#

Tentang Dataset#

Dataset berikut digunakan untuk memprediksi apakah calon peminjam memenuhi syarat untuk disetujui peminjamannya berdasarkan wilayah, keuangan, dan faktor yang berhubungan dengan kredit lainnta. Dataset ini cocok untuk klasifikasi menggunakan machine learning.

Dataset diperoleh dari repository Kaggle pada link berikut

https://www.kaggle.com/datasets/avineshprabhakaran/loan-eligibility-prediction

Dataset memiliki cakupan data sebagai berikut

Column |

Description |

Example |

|---|---|---|

Customer_ID |

Unique identifier for each loan applicant |

569 |

Gender |

Gender of the applicant |

Male / Female |

Married |

Marital status of the applicant |

Yes / No |

Dependents |

Number of dependents |

0, 1, 2, 3 |

Education |

Education level of the applicant |

Graduate / Not Graduate |

Self_Employed |

Whether the applicant is self-employed |

Yes / No |

Applicant_Income |

Applicant’s monthly income |

5000 |

Coapplicant_Income |

Coapplicant’s monthly income |

1500 |

Loan_Amount |

Loan amount requested (in thousands) |

128 |

Loan_Amount_Term |

Loan repayment term (in months) |

360 |

Credit_History |

Credit history meets lending criteria |

(1 = Yes, 0 = No) 1 |

Property_Area |

Type of property area |

Urban / Semiurban / Rural |

Loan_Status |

Loan approved or not (target variable) |

Y / N |

Import the library#

[1]:

import kagglehub

import os

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.ticker import MultipleLocator

import matplotlib as mpl

import seaborn as sns

Unduh Dataset#

[2]:

path = kagglehub.dataset_download("avineshprabhakaran/loan-eligibility-prediction")

filename = os.listdir(path)[0]

fullpath = "/".join([path,filename])

fullpath

Downloading to /root/.cache/kagglehub/datasets/avineshprabhakaran/loan-eligibility-prediction/3.archive...

100%|██████████| 7.39k/7.39k [00:00<00:00, 13.1MB/s]

Extracting files...

[2]:

'/root/.cache/kagglehub/datasets/avineshprabhakaran/loan-eligibility-prediction/versions/3/Loan Eligibility Prediction.csv'

Set the default plot style#

[3]:

def DefaultPlotStyle():

plt.rcParams['lines.linewidth'] = 2

plt.rcParams['lines.linestyle'] = '-'

plt.rcParams['figure.figsize'] = [12,10]

plt.rcParams['font.size'] = 12

DefaultPlotStyle()

Membaca Dataset#

[4]:

df = pd.read_csv(fullpath)

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 614 entries, 0 to 613

Data columns (total 13 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Customer_ID 614 non-null int64

1 Gender 614 non-null object

2 Married 614 non-null object

3 Dependents 614 non-null int64

4 Education 614 non-null object

5 Self_Employed 614 non-null object

6 Applicant_Income 614 non-null int64

7 Coapplicant_Income 614 non-null float64

8 Loan_Amount 614 non-null int64

9 Loan_Amount_Term 614 non-null int64

10 Credit_History 614 non-null int64

11 Property_Area 614 non-null object

12 Loan_Status 614 non-null object

dtypes: float64(1), int64(6), object(6)

memory usage: 62.5+ KB

Pengecekan Dataset#

[5]:

# Checking missing value

df.isnull().sum().reset_index().T

[5]:

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| index | Customer_ID | Gender | Married | Dependents | Education | Self_Employed | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Property_Area | Loan_Status |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

Tidak ada data atau nilai yang kosong dalam dataset ini

[6]:

# Checking duplicate data

any(df.duplicated())

[6]:

False

[7]:

# Checking duplicate customer id

df['Customer_ID'].value_counts().reset_index().sort_values(by='count', ascending=False).head()

[7]:

| Customer_ID | count | |

|---|---|---|

| 613 | 271 | 1 |

| 0 | 606 | 1 |

| 1 | 569 | 1 |

| 2 | 15 | 1 |

| 3 | 95 | 1 |

Tidak ada data yang duplikat dalam dataset ini

Tampilan Dataset#

[8]:

df.head()

[8]:

| Customer_ID | Gender | Married | Dependents | Education | Self_Employed | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Property_Area | Loan_Status | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 569 | Female | No | 0 | Graduate | No | 2378 | 0.0 | 9 | 360 | 1 | Urban | N |

| 1 | 15 | Male | Yes | 2 | Graduate | No | 1299 | 1086.0 | 17 | 120 | 1 | Urban | Y |

| 2 | 95 | Male | No | 0 | Not Graduate | No | 3620 | 0.0 | 25 | 120 | 1 | Semiurban | Y |

| 3 | 134 | Male | Yes | 0 | Graduate | Yes | 3459 | 0.0 | 25 | 120 | 1 | Semiurban | Y |

| 4 | 556 | Male | Yes | 1 | Graduate | No | 5468 | 1032.0 | 26 | 360 | 1 | Semiurban | Y |

Analisis Parameter#

[9]:

# Creating object feature for Credit History

mapper = lambda x : "YES" if x == 1 else "NO"

df['Credit_History_Obj'] = df['Credit_History'].map(mapper)

df.head()

[9]:

| Customer_ID | Gender | Married | Dependents | Education | Self_Employed | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Property_Area | Loan_Status | Credit_History_Obj | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 569 | Female | No | 0 | Graduate | No | 2378 | 0.0 | 9 | 360 | 1 | Urban | N | YES |

| 1 | 15 | Male | Yes | 2 | Graduate | No | 1299 | 1086.0 | 17 | 120 | 1 | Urban | Y | YES |

| 2 | 95 | Male | No | 0 | Not Graduate | No | 3620 | 0.0 | 25 | 120 | 1 | Semiurban | Y | YES |

| 3 | 134 | Male | Yes | 0 | Graduate | Yes | 3459 | 0.0 | 25 | 120 | 1 | Semiurban | Y | YES |

| 4 | 556 | Male | Yes | 1 | Graduate | No | 5468 | 1032.0 | 26 | 360 | 1 | Semiurban | Y | YES |

[10]:

# Selecting only object features

object_list = df.select_dtypes(include=['object']).columns

object_list

[10]:

Index(['Gender', 'Married', 'Education', 'Self_Employed', 'Property_Area',

'Loan_Status', 'Credit_History_Obj'],

dtype='object')

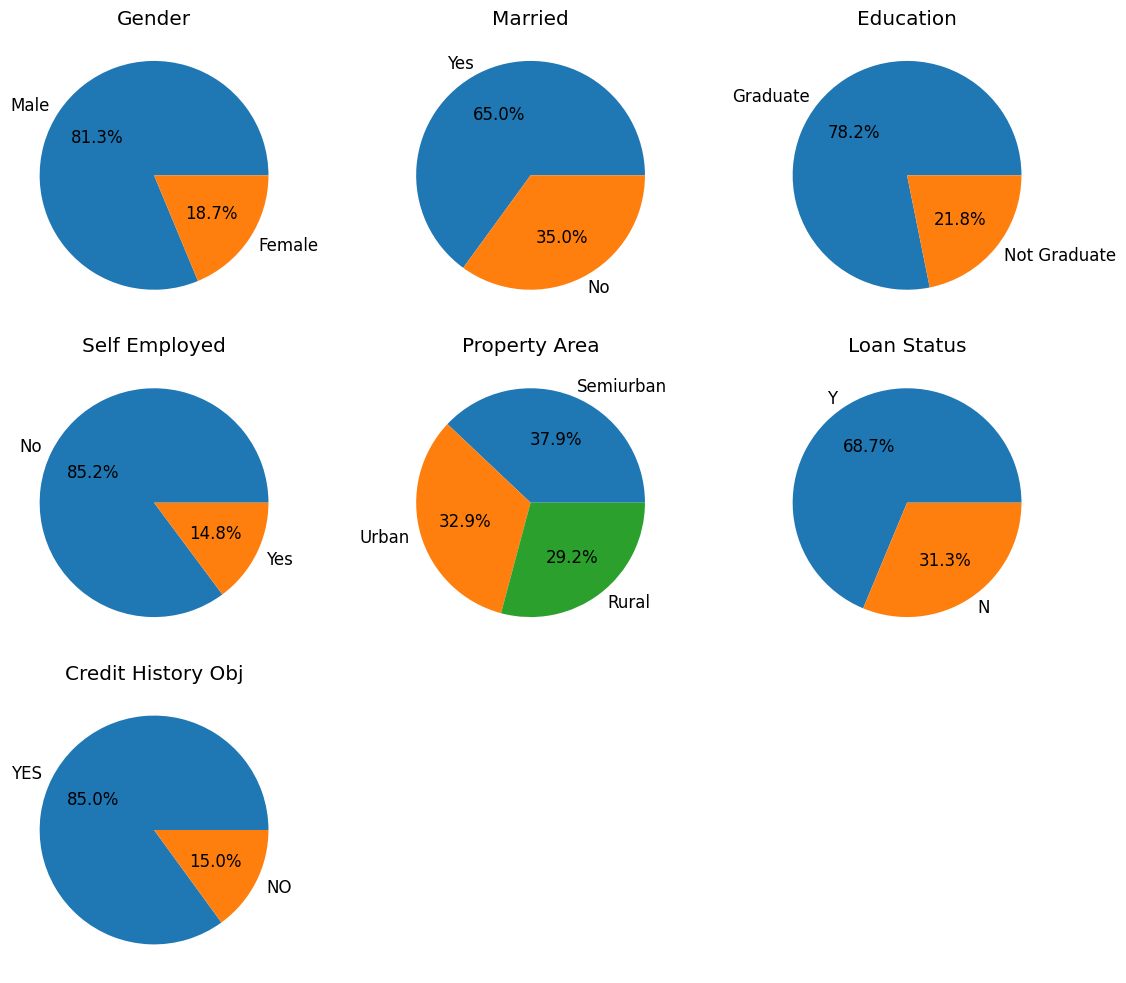

[11]:

# Plotting object features

ndata = df.shape[0]

nobject = len(object_list)

n_cols = 3

n_rows = (nobject // n_cols) + 1

fig, ax = plt.subplots(nrows=n_rows, ncols=n_cols)

ax_flat = ax.flatten()

for i, ax in enumerate(ax_flat):

if i < nobject:

df_obj = df[object_list[i]].value_counts().reset_index()

df_obj['percentage'] = (df_obj['count']/df_obj['count'].sum()) * 100

ax = ax_flat[i]

ax.pie(df_obj['percentage'], labels=df_obj[object_list[i]], autopct="%.1f%%")

ax.set_title(object_list[i].replace("_", " "))

else:

ax.axis('off')

plt.tight_layout()

[12]:

# Calculating the total income from the applicant income and co-applicant income

df['Total_Income'] = df['Applicant_Income'] + df['Coapplicant_Income']

df.head()

[12]:

| Customer_ID | Gender | Married | Dependents | Education | Self_Employed | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Property_Area | Loan_Status | Credit_History_Obj | Total_Income | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 569 | Female | No | 0 | Graduate | No | 2378 | 0.0 | 9 | 360 | 1 | Urban | N | YES | 2378.0 |

| 1 | 15 | Male | Yes | 2 | Graduate | No | 1299 | 1086.0 | 17 | 120 | 1 | Urban | Y | YES | 2385.0 |

| 2 | 95 | Male | No | 0 | Not Graduate | No | 3620 | 0.0 | 25 | 120 | 1 | Semiurban | Y | YES | 3620.0 |

| 3 | 134 | Male | Yes | 0 | Graduate | Yes | 3459 | 0.0 | 25 | 120 | 1 | Semiurban | Y | YES | 3459.0 |

| 4 | 556 | Male | Yes | 1 | Graduate | No | 5468 | 1032.0 | 26 | 360 | 1 | Semiurban | Y | YES | 6500.0 |

[13]:

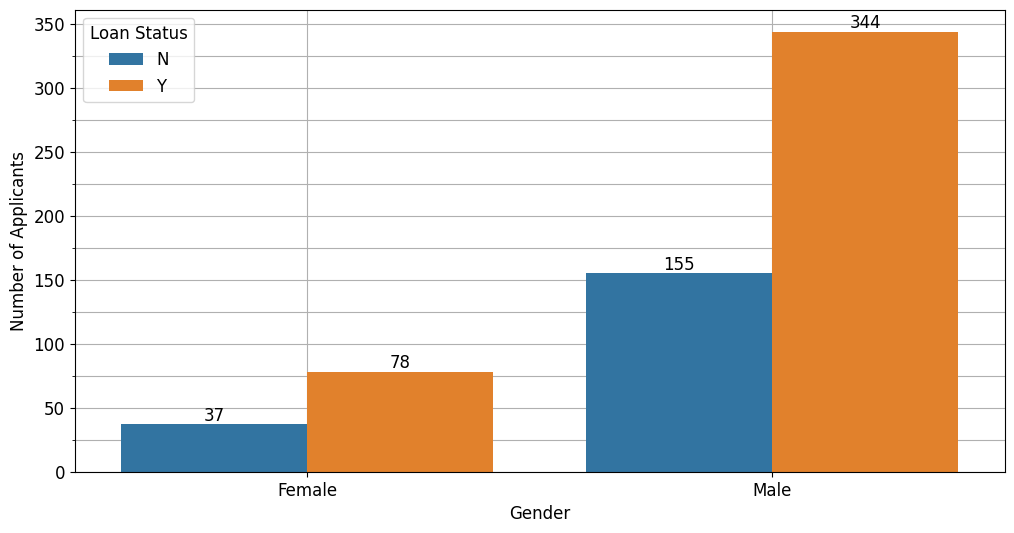

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Gender', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

plt.legend(title='Loan Status')

ax.set_axisbelow(True)

Berdasarkan jenis kelamin, peminjaman yang berhasil dilakukan secara mayoritas oleh pelanggan laki-kali, hanya kurang dari 100 pelanggan wanita yang berhasil mendapatkan pinjaman.

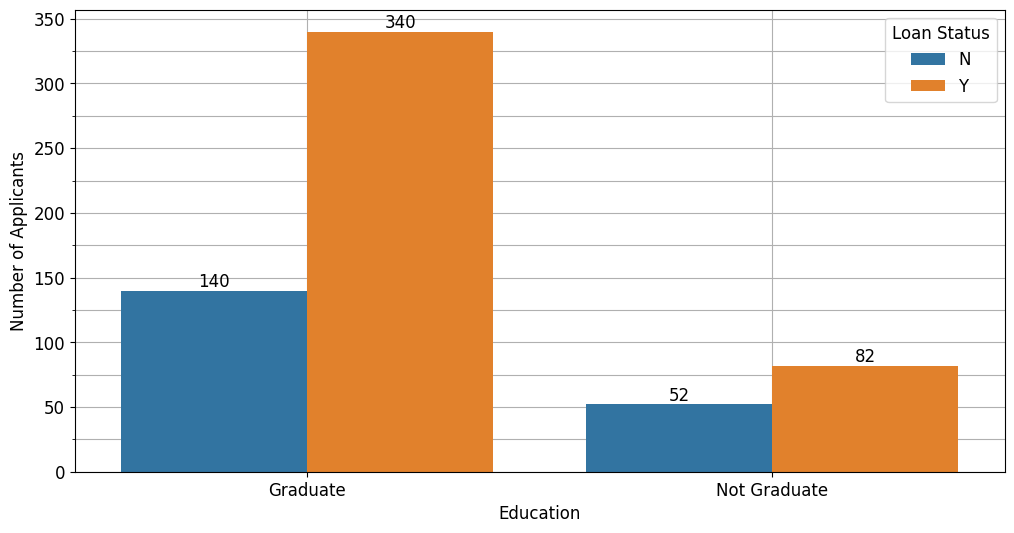

[14]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Education',hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

plt.legend(title='Loan Status')

ax.set_axisbelow(True)

Berdasarkan status pendidikan, pelanggan yang lulus kuliah lebih berpeluang menerima pinjaman dibandingkan dengan pelanggan yang tidak lulus kuliah.

[15]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Self_Employed', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

plt.legend(title='Loan Status')

ax.set_axisbelow(True)

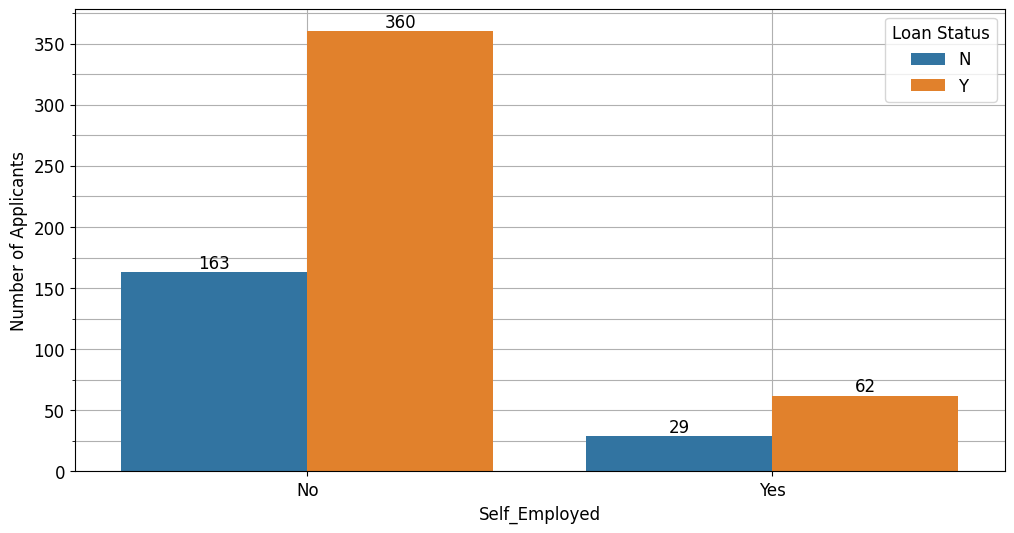

Berdasarkan status pekerjaan, pelanggan dengan status bukan wiraswasta berpeluang mendapatkan pinjaman.

[16]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Property_Area', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

ax.set_axisbelow(True)

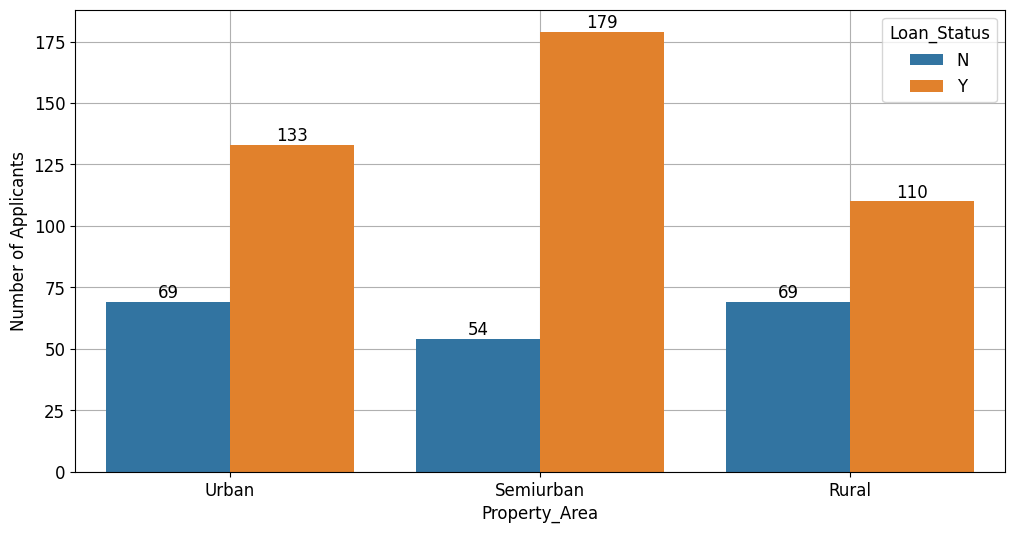

Berdasarkan wilayah tempat tinggal, peminjaman banyak diajukan oleh pelanggan yang tinggal di wilayah semiurban, diikuti dengan pelanggan yang tinggal di wilayah urban dan pedesaan.

[17]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Dependents', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

ax.set_axisbelow(True)

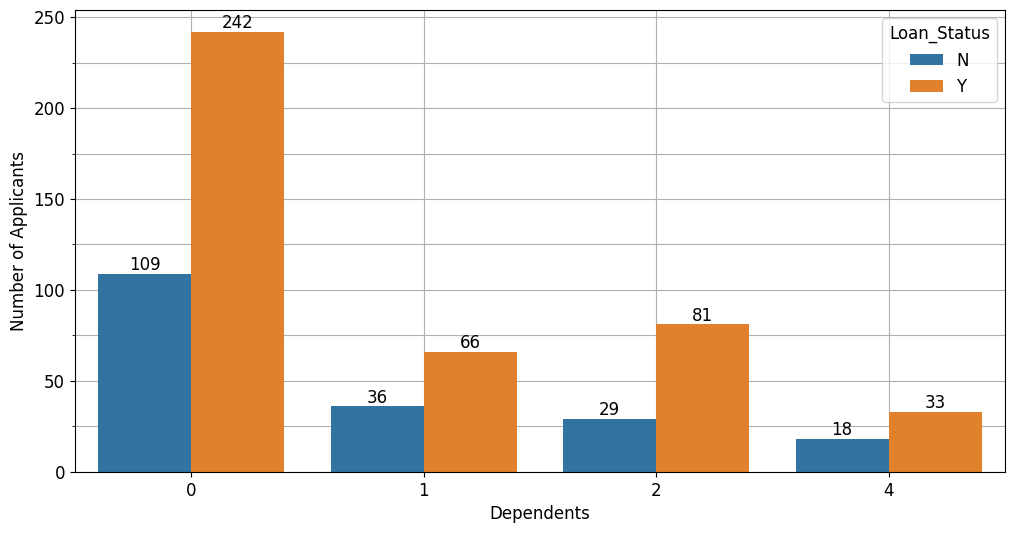

Mayoritas peminjaman yang diajukan dan diterima berasal dari pelanggan yang tidak memiliki tanggungan.

[18]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Married', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

ax.set_axisbelow(True)

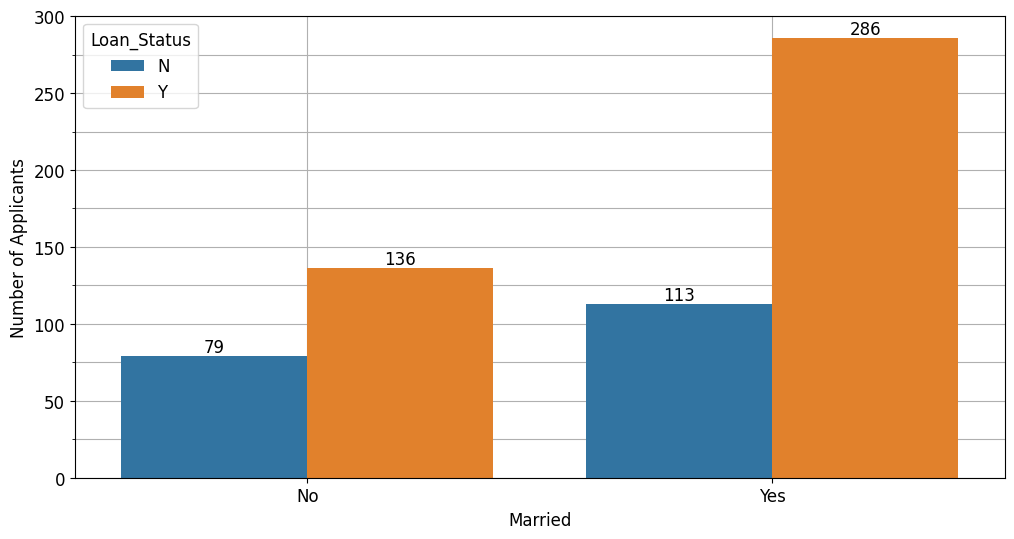

Berdasarkan status pernikahan, pelanggan dengan status sudah menikah berpeluang menerima pinjaman.

[20]:

fig, ax = plt.subplots(figsize=(12,6))

sns.countplot(data=df, x='Credit_History_Obj', hue='Loan_Status', ax=ax)

for container in ax.containers:

ax.bar_label(container, label_type='edge')

# ax.set_ylim([0,200])

ax.set_ylabel('Number of Applicants')

ax.yaxis.set_minor_locator(MultipleLocator(25))

plt.grid(which='both')

ax.set_axisbelow(True)

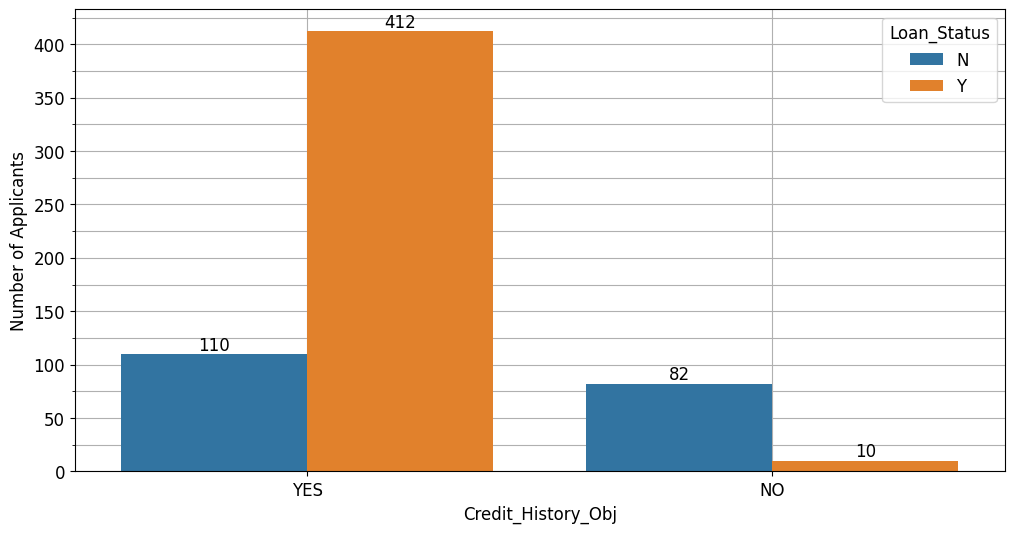

Berdasarkan rekam jejak peminjaman, pelanggan yang pernah melakukan peminjaman berpeluang mendapatkan pinjaman kembali.

[21]:

# Selecting only numeric data

numeric_list = df.select_dtypes(exclude=['object']).columns

numeric_list = numeric_list.delete(0)

numeric_list

[21]:

Index(['Dependents', 'Applicant_Income', 'Coapplicant_Income', 'Loan_Amount',

'Loan_Amount_Term', 'Credit_History', 'Total_Income'],

dtype='object')

[22]:

df_numeric = df.select_dtypes(exclude=['object'])

df_numeric.head()

[22]:

| Customer_ID | Dependents | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Total_Income | |

|---|---|---|---|---|---|---|---|---|

| 0 | 569 | 0 | 2378 | 0.0 | 9 | 360 | 1 | 2378.0 |

| 1 | 15 | 2 | 1299 | 1086.0 | 17 | 120 | 1 | 2385.0 |

| 2 | 95 | 0 | 3620 | 0.0 | 25 | 120 | 1 | 3620.0 |

| 3 | 134 | 0 | 3459 | 0.0 | 25 | 120 | 1 | 3459.0 |

| 4 | 556 | 1 | 5468 | 1032.0 | 26 | 360 | 1 | 6500.0 |

[23]:

df_numeric.drop('Customer_ID', axis=1, inplace=True)

df_numeric.head()

[23]:

| Dependents | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Total_Income | |

|---|---|---|---|---|---|---|---|

| 0 | 0 | 2378 | 0.0 | 9 | 360 | 1 | 2378.0 |

| 1 | 2 | 1299 | 1086.0 | 17 | 120 | 1 | 2385.0 |

| 2 | 0 | 3620 | 0.0 | 25 | 120 | 1 | 3620.0 |

| 3 | 0 | 3459 | 0.0 | 25 | 120 | 1 | 3459.0 |

| 4 | 1 | 5468 | 1032.0 | 26 | 360 | 1 | 6500.0 |

[24]:

df.describe()

[24]:

| Customer_ID | Dependents | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Total_Income | |

|---|---|---|---|---|---|---|---|---|

| count | 614.000000 | 614.000000 | 614.000000 | 614.000000 | 614.000000 | 614.000000 | 614.000000 | 614.000000 |

| mean | 307.500000 | 0.856678 | 5403.459283 | 1621.245798 | 142.022801 | 338.892508 | 0.850163 | 7024.705081 |

| std | 177.390811 | 1.216651 | 6109.041673 | 2926.248369 | 87.083089 | 69.716355 | 0.357203 | 6458.663872 |

| min | 1.000000 | 0.000000 | 150.000000 | 0.000000 | 9.000000 | 12.000000 | 0.000000 | 1442.000000 |

| 25% | 154.250000 | 0.000000 | 2877.500000 | 0.000000 | 98.000000 | 360.000000 | 1.000000 | 4166.000000 |

| 50% | 307.500000 | 0.000000 | 3812.500000 | 1188.500000 | 125.000000 | 360.000000 | 1.000000 | 5416.500000 |

| 75% | 460.750000 | 2.000000 | 5795.000000 | 2297.250000 | 164.750000 | 360.000000 | 1.000000 | 7521.750000 |

| max | 614.000000 | 4.000000 | 81000.000000 | 41667.000000 | 700.000000 | 480.000000 | 1.000000 | 81000.000000 |

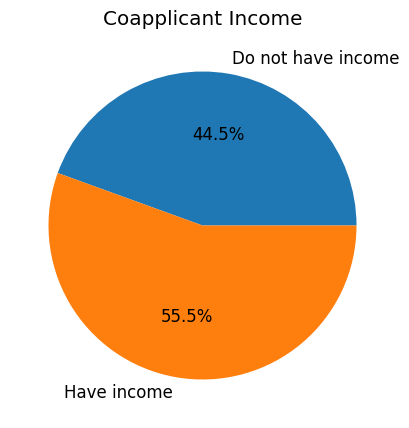

[25]:

number_Coapplicant_Income_zero = df[df['Coapplicant_Income'] == 0].shape[0]

number_Coapplicant_Income_nonzero = df.shape[0] - number_Coapplicant_Income_zero

percentage_Coapplicant_Income_zero = (number_Coapplicant_Income_zero/df.shape[0])*100

percentage_Coapplicant_Income_nonzero = (number_Coapplicant_Income_nonzero/df.shape[0])*100

fig, ax = plt.subplots(figsize=(5,5))

ax.pie(x= [percentage_Coapplicant_Income_zero, percentage_Coapplicant_Income_nonzero],

labels=['Do not have income', 'Have income'],

autopct="%.1f%%");

ax.set_title('Coapplicant Income')

[25]:

Text(0.5, 1.0, 'Coapplicant Income')

[26]:

# Encoding the object data to numeric

df_object = df.select_dtypes(include=['object'])

df_object.head()

[26]:

| Gender | Married | Education | Self_Employed | Property_Area | Loan_Status | Credit_History_Obj | |

|---|---|---|---|---|---|---|---|

| 0 | Female | No | Graduate | No | Urban | N | YES |

| 1 | Male | Yes | Graduate | No | Urban | Y | YES |

| 2 | Male | No | Not Graduate | No | Semiurban | Y | YES |

| 3 | Male | Yes | Graduate | Yes | Semiurban | Y | YES |

| 4 | Male | Yes | Graduate | No | Semiurban | Y | YES |

[27]:

gender_encoder = lambda x : 1 if x == 'Male' else 0

married_encoder = lambda x : 1 if x == 'Yes' else 0

education_encoder = lambda x : 1 if x == 'Graduate' else 0

self_employed_encoder = lambda x : 1 if x == 'Yes' else 0

property_area_encoder = lambda x : 1 if x == 'Urban' else 2 if x == 'Semiurban' else 3

loan_status_encoder = lambda x : 1 if x == 'Y' else 0

mappers = [gender_encoder, married_encoder, education_encoder, self_employed_encoder, property_area_encoder, loan_status_encoder]

df_object_names = df_object.columns.to_list()

df_object_names.remove('Credit_History_Obj')

df_object_names

[27]:

['Gender',

'Married',

'Education',

'Self_Employed',

'Property_Area',

'Loan_Status']

[28]:

df_duplicate = df.copy(deep=True)

for i, obj in enumerate(df_object_names):

df_duplicate[obj] = df_duplicate[obj].map(mappers[i])

df_duplicate.drop(['Customer_ID','Credit_History_Obj'], axis=1, inplace=True)

[29]:

df_duplicate.head()

[29]:

| Gender | Married | Dependents | Education | Self_Employed | Applicant_Income | Coapplicant_Income | Loan_Amount | Loan_Amount_Term | Credit_History | Property_Area | Loan_Status | Total_Income | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 0 | 0 | 1 | 0 | 2378 | 0.0 | 9 | 360 | 1 | 1 | 0 | 2378.0 |

| 1 | 1 | 1 | 2 | 1 | 0 | 1299 | 1086.0 | 17 | 120 | 1 | 1 | 1 | 2385.0 |

| 2 | 1 | 0 | 0 | 0 | 0 | 3620 | 0.0 | 25 | 120 | 1 | 2 | 1 | 3620.0 |

| 3 | 1 | 1 | 0 | 1 | 1 | 3459 | 0.0 | 25 | 120 | 1 | 2 | 1 | 3459.0 |

| 4 | 1 | 1 | 1 | 1 | 0 | 5468 | 1032.0 | 26 | 360 | 1 | 2 | 1 | 6500.0 |

Applying Logistic Regression#

[30]:

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import train_test_split

from sklearn.metrics import confusion_matrix, accuracy_score, classification_report, roc_curve, roc_auc_score

from sklearn.preprocessing import StandardScaler

import numpy as np

[31]:

target = df_duplicate['Loan_Status']

features = df_duplicate.drop('Loan_Status', axis=1)

# Splitting the dataset, the test dataset is 20% of the total dataset

X_train, X_test, y_train, y_test = train_test_split(features, target, test_size=0.2, random_state=42)

# Applying the standar scaler for the scaling unbalance scale of dataset

scaler = StandardScaler()

X_train_scaled = scaler.fit_transform(X_train)

X_test_scaled = scaler.transform(X_test)

# Applying the logistic regression

linreg_model = LogisticRegression()

linreg_model.fit(X_train_scaled,y_train)

# Predicting the test dataset (scaled)

y_pred = linreg_model.predict(X_test_scaled)

# Evaluating the accuracy of the model

print(f"Accuracy: {accuracy_score(y_pred, y_test)}")

Accuracy: 0.8211382113821138

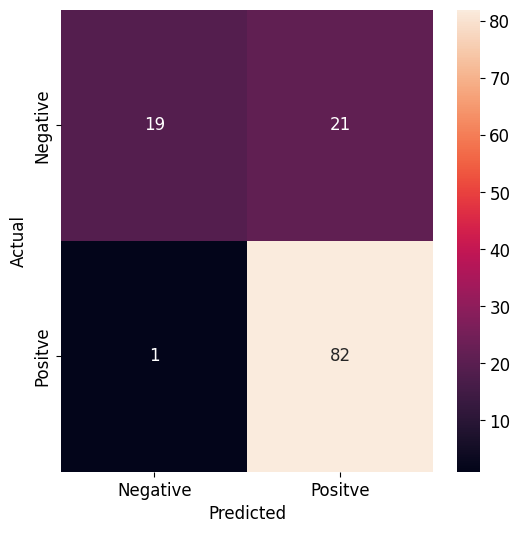

[32]:

# Providing the confusion matrix

# true negatives is C_{0,0},

# false positives is C_{0,1},

# false negatives is C_{1,0},

# true positives is C_{1,1}

custom_x_labels = ['Negative', 'Positve']

custom_y_labels = ['Negative', 'Positve']

fig, ax = plt.subplots(figsize=(6,6))

sns.heatmap(confusion_matrix(y_test, y_pred),

xticklabels=custom_x_labels,

yticklabels=custom_y_labels,

annot=True,

ax=ax)

ax.set_xlabel('Predicted')

ax.set_ylabel('Actual')

[32]:

Text(41.722222222222214, 0.5, 'Actual')

[33]:

# Generating the classification report

print(classification_report(y_pred, y_test, target_names=['Loan Status-No', 'Loan Status-Yes']));

precision recall f1-score support

Loan Status-No 0.47 0.95 0.63 20

Loan Status-Yes 0.99 0.80 0.88 103

accuracy 0.82 123

macro avg 0.73 0.87 0.76 123

weighted avg 0.90 0.82 0.84 123

Akurasi model sekitar 82% untuk memprediksi target (status peminjaman). Model ini cocok untuk memprediksi target sebenarnya (status pinjaman yang dapat diterima) sensitivitas (recall) 80%, tetapi lebih sensitif untuk memprediksi target status pinjaman yang tidak dapat diterima. Namun, model ini mampu memprediksi status pinjaman yang dapat diterima dengan presisi 99%.

[34]:

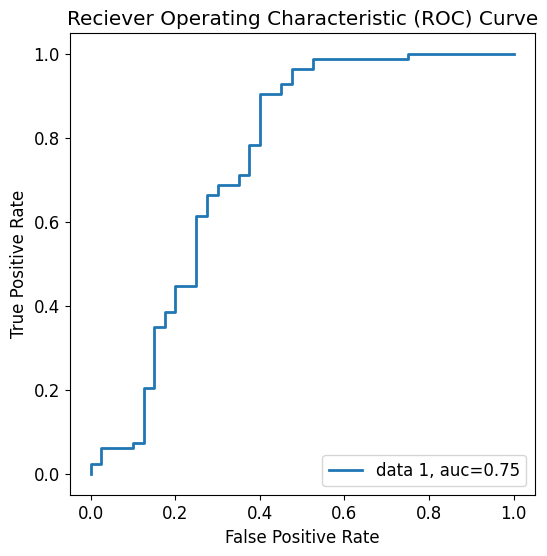

# Plotting the ROC curve

y_pred_proba = linreg_model.predict_proba(X_test_scaled)[::,1]

fpr, tpr, _ = roc_curve(y_test, y_pred_proba)

auc = roc_auc_score(y_test, y_pred_proba)

fig, ax = plt.subplots(figsize=(6,6))

ax.plot(fpr,tpr,label=f"data 1, auc={auc:.2f}")

ax.set_xlabel('False Positive Rate')

ax.set_ylabel('True Positive Rate')

ax.set_title('Reciever Operating Characteristic (ROC) Curve')

plt.legend(loc=4)

plt.show()